Consumers are perhaps more committed than ever to better money management and improving their finances. In fact, the top three goals among consumers according to survey data in 2023 are to increase savings (41%), cut costs (41%), and pay off debt (35%).

The reality is that members of your community need information and resources about how to manage money, make buying decisions, search for and obtain loans for major purchases, and more. They’re looking to you—their trusted financial services provider—to guide them through what can be incredibly complicated. Financial institutions have a huge opportunity to tune into customer needs and expectations, and meet them where they are to attract and retain loyal customers. When you do, you’re able to reap tons of tangible benefits.

The Advantages of Being a Resource

Whether you’re looking to better reach and engage Gen Z or looking to find your way to the top of Google search results for specific products and services—serving as a resource for info about finances and money management can certainly help. When you provide the information people are looking for, you add value to potential customers’ lives in a way that builds trust and generates new business.

Sometimes it’s as easy as knowing what people don’t know or need help with, and responding to it using content. “When you’re answering the questions people have about managing their money and finances through content on your social media channels, on your website, et cetera–you’re reaching people with the information they want, on the channels they frequent,” says Social Assurance’s Ben Pankonin, who works with community banks, credit unions, and financial brands all over the country to create and execute effective content marketing.

On your website, this might look like long-form content—perhaps a blog that helps folks navigate a commercial loan for a specific type of industry, a refi or mortgage loan, or even an auto or recreational vehicle loan. The (perhaps cold) reality is that you likely don’t have a cohort of people checking your website regularly for the latest blog update. However, you do likely have folks in your area searching online for common and often quite specific questions about finances, loans, major asset purchases, interest rates, saving for college, retirement, and other important financial matters. If your website puts out timely and relevant content that addresses these key questions, it’s likely to be served up when folks are Googling.

While it’s tough to create a consistent following of website visitors, it’s a bit easier to build an audience through social channels. Indeed, these platforms are designed to help you capture the attention of people who have opted into following your page and want to receive your content. For these reasons and more, social media is another great place to position your organization as a trusted resource for financial information. Consider a video series or a recurring ask-the-expert post. Better yet, look for ways to tie your social posts into longer-form content on your website, so you can capture the interest of potential customers, drive them back to your website, and convert them into a lead.

What to Post About

So, you might be wondering: That all sounds great, but what should we be posting about? You might be surprised by how much guidance and information customers are looking for about things you may think are common knowledge. Here’s a quick list of topics to consider posting about during the month of April and beyond.

- What’s a CD and how does it work?

- What’s a High Yield Savings account? Who are they for? What do you need to get started?

- Can I get a loan for an RV, boat, or other summer vehicle? How?

- When’s the best time to buy a house?

- How can I teach my grade-school, teenagers, or college-age kids about saving, budgeting, and investing?

- How do HELOCs work and what are they for?

- What paperwork and documentation is needed for a small business loan?

- What’s the difference between taking out a line of credit and a small business loan to launch my latest business idea?

- How much money should I have saved for retirement?

- How do I make a household budget?

Grab & Go Content

We’ve pulled together some free, downloadable posts for community banks, credit unions, and financial brands to use in full or as a starting point in honor of Financial Literacy Month and beyond.

Need some graphics to go with your content options? The Social Assurance content team has your back. Click the link below to download all the graphics in one click!

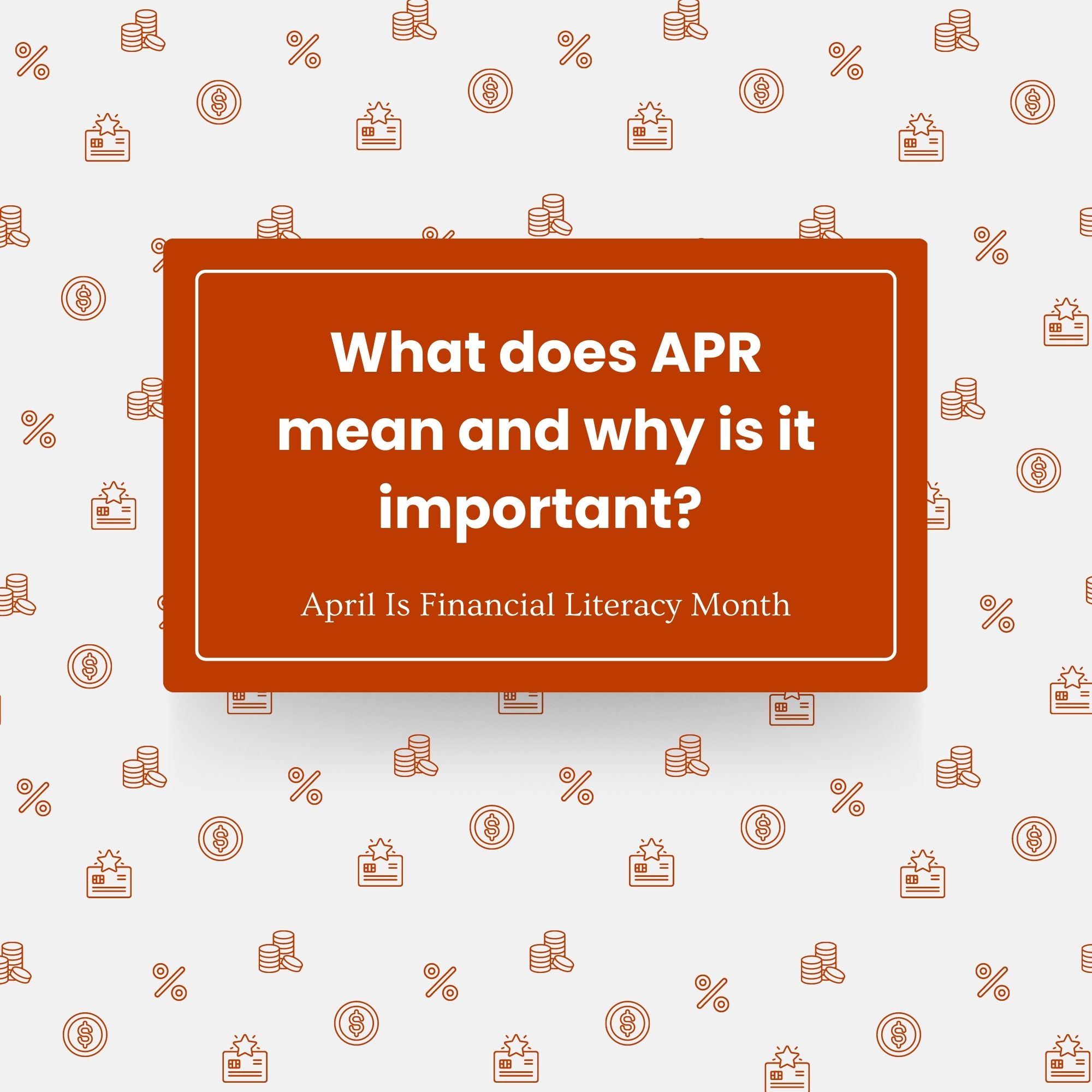

What does APR mean and why is it important?

Your APR (Annual Percentage Rate) represents the total cost of borrowing money, including interest and fees, and is a crucial factor in determining the affordability of loans and credit cards. By knowing your APR, you can make informed decisions about borrowing and avoid high-interest debt.

#FinancialLiteracyMonth #BorrowSmart

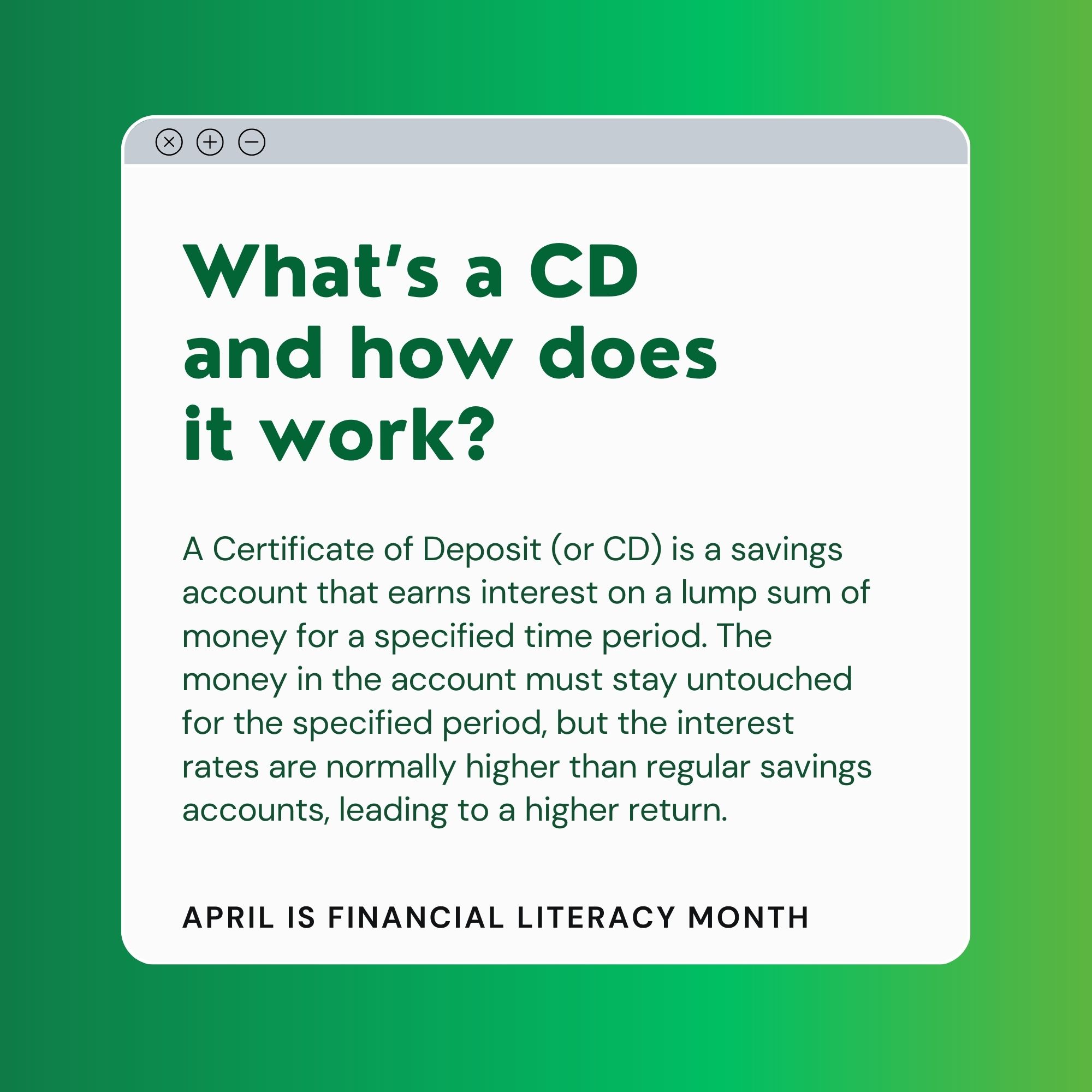

What’s a CD and how does it work?

A Certificate of Deposit (or CD) is a savings account that earns interest on a lump sum of money for a specified time period. The money in the account must stay untouched for the specified period, but the interest rates are normally higher than regular savings accounts, leading to a higher return. If you’re looking for a secure investment option with a guaranteed return, a CD could be the right fit for you!

#FinancialLiteracyMonth #SavingsGoals

How can I teach my grade-school, teenagers, or college-age kids about saving and budgeting?

Start young! Take the first step and open your child a savings account that you can help them manage by tracking deposits and purchases. Allow them to earn their own money, and aid them in creating a mock budget. Aside from telling your children about important financial topics, hands-on-learning is a big help as well.

#FinancialLiteracyMonth #TeachKidsToSave

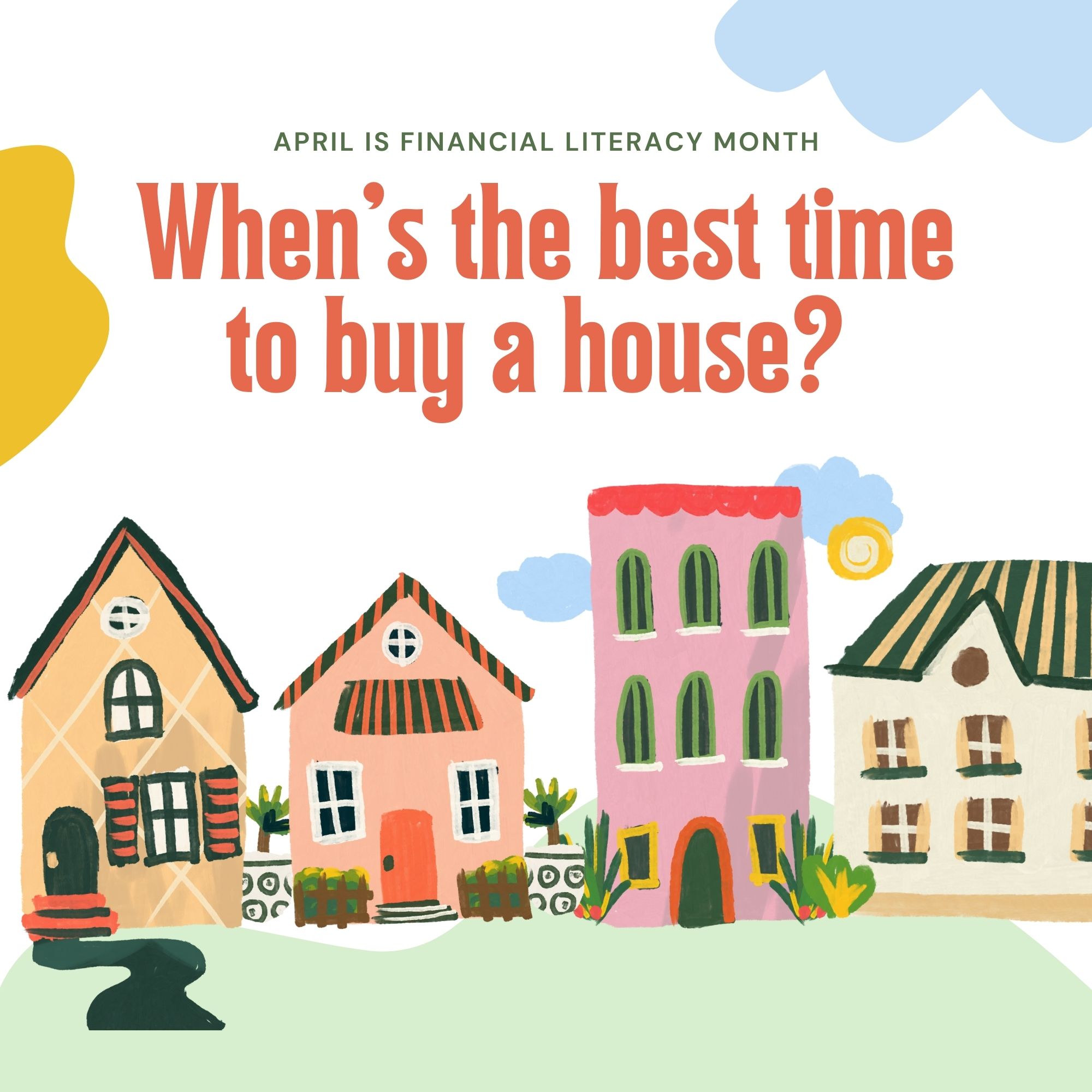

When’s the best time to buy a house?

Short answer: there isn’t necessarily one. The cheapest time to buy a house is often in winter, as less listings mean less buyers in the winter months—making sellers eager to close a deal. Homeowners are more likely to list their homes in the spring, meaning more competitive prices and potential buyers—but also more options. What really matters are your needs and finances. The best time to buy a home is when you’re financially stable, likely to get approved for a loan, and ready to take the leap!

#FinancialLiteracyMonth #HomeOwnership

How do HELOCs work and what are they for?

A Home Equity Line of Credit (or HELOC) is a financial tool that allows you to borrow money against the value of your home. By taking out a HELOC, you can use the equity you’ve built up in your home to pay for expenses like your child’s tuition, home renovations, or unexpected costs. When you apply for a HELOC, you are approved for a certain amount of credit and can borrow against it as needed, making monthly payments. Utilizing the equity in your home through a HELOC can be a useful strategy for managing your finances and achieving your financial goals!

#FinancialLiteracyMonth #MoneyTips

What affects credit score?

Your credit score is a numerical representation of your creditworthiness and is used by lenders to determine the likelihood of you repaying a loan. Having a good credit score can help you qualify for better loan terms, lower interest rates, and higher credit limits.

Several factors affect your credit score, including your payment history, credit utilization ratio, length of credit history, types of credit used, and recent credit inquiries. By maintaining a positive payment history, keeping your credit utilization low, and having a mix of credit types, you can improve your credit score and secure better financial opportunities!

#FinancialLiteracyMonth #CreditEducation

How do student loans work?

If you’re considering how to finance your education, student loans may be a viable option for you. To apply for a student loan, you must first submit an application and wait for approval. Once approved, you’ll receive the loan funds, which you’ll pay back over time with interest. Although interest rates can vary, they are generally lower than those of other types of loans. Many student loans offer a grace period after graduation, which means you won’t have to make payments during this time. However, interest may still accumulate during the grace period, so it’s important to be aware of the terms and conditions.

#FinancialLiteracyMonth #CollegeFinance

When should I start saving for retirement & how much should I save?

Starting to save for retirement early can be a wise decision, as it allows your money more time to grow. It is generally recommended to save at least 10-15% of your gross income for retirement, as a rule of thumb. However, the exact amount you should save may vary based on your retirement goals and current expenses. By saving diligently and planning for your retirement goals, you can help ensure a comfortable financial future!

#FinancialLiteracyMonth #RetirementReady

Investing Basics

If you’re new to investing, it’s essential to begin with the fundamentals. The first step is to determine your investment goals and your risk tolerance. Next, you should consider spreading your investments across different asset classes, such as stocks, bonds, and real estate, to diversify your portfolio. Investing comes with risk, but with careful strategies and a long-term perspective, it can be a valuable tool for building wealth.

#FinancialLiteracyMonth #InvestingBasics

How do I make a household budget?

Creating a household budget is a fundamental step in managing your finances effectively. Here are four steps to get started!

- Gather all your financial information, including your income and expenses.

- Prioritize your spending by identifying essential expenses, such as housing, food, and utilities, and discretionary expenses, such as entertainment and dining out.

- Create a budget that reflects your financial goals and allows you to save money each month.

- Track your expenses regularly and adjust your budget as needed.

By taking control of your finances through budgeting, you can achieve greater financial stability and peace of mind.

#FinancialLiteracyMonth #BudgetingTips

Can I get a loan for an RV, boat, or other summer vehicle? How?

You CAN get a loan for an RV, boat, or other recreational vehicle. To get started, you’ll submit a loan application, which will require information such as your income, credit score, and the amount you’re looking to borrow.

The lender will then review your application and determine if you meet their criteria. If approved, you’ll receive a loan offer that outlines the loan amount, interest rate, repayment terms, and any associated fees.

Consider working with a loan specialist who can help you understand your options and guide you through the application process. Remember to also factor in the ongoing costs of owning and maintaining the vehicle, such as insurance, fuel, and storage fees!

#FinancialLiteracyMonth #SummerFun

Take the Next Steps on Social

Certainly April is financial literacy month, but it’s not the only time community banks, credit unions, and financial brands can (and should!) serve as a resource. In fact, social media is a great way to leverage consumer interest in knowing how to better manage money and finances to build trust, generate business from under-banked customers, and grow deposits overall.

Need a hand better utilizing your bank’s social media channels or even just producing content? Social Assurance is here to help. Follow the link below to learn more.