April is Financial Literacy Month and is the perfect time to educate individuals and businesses about important financial concepts and topics. This toolkit comes with a variety of posts that can be used as inspiration, supplemental content, or across all your organization’s social channels over the course of the month. Click the download button to get the graphics—then simply copy and paste the corresponding text to complete your posts.

FDIC

You can feel confident knowing your money is protected when it’s kept at an FDIC insured community bank! The Federal Deposit Insurance Corporation (FDIC) insures deposits at participating banks. Here’s how that protection works:

✅ Coverage Limit: Insures deposits up to $250,000 per depositor, per insured bank, per ownership category.

✅ What’s Covered? Checking accounts, savings accounts, money market deposit accounts, and CDs—your standard deposit accounts.

✅ What’s NOT Covered? Investments like stocks, bonds, mutual funds, crypto assets, or life insurance policies.

✅ How to Confirm Coverage? Visit the FDIC website to verify your bank is federally insured.

As long as your community bank is FDIC-insured, your deposits are protected with built-in federal coverage!

#FDIC #CommunityBanking #FinancialEducation

NCUA

You can feel confident knowing your money is protected when it’s kept at an NCUA-insured credit union! The NCUA (National Credit Union Administration) protects deposits at federally insured credit unions helping safeguard members’ money. Here’s what to know:

✅ Coverage Limit: Insures deposits up to $250,000 per member, per insured credit union, per ownership category.

✅ What’s Covered? Checking accounts, savings accounts, money market accounts, and CDs—your standard share deposit accounts.

✅ What’s NOT Covered? Investments like stocks, bonds, mutual funds, crypto assets, or life insurance policies.

✅ How to Confirm Coverage? Visit the NCUA website to verify your credit union is federally insured.

As long as your credit union is NCUA-insured, your deposits are protected with built-in federal coverage!

CD

Looking for a low-risk way to grow your savings? A Certificate of Deposit (CD) might be worth considering! A CD is a type of savings account offered by community banks and credit unions. With a CD, you agree to keep your money in the account for a specific period of time and in exchange you earn interest.

Characteristics of a CD:

📈 Fixed Term: You choose how long your money stays in the CD—from a few months to several years.

📈Guaranteed Rate: Your interest rate is locked in for the full term, even if market rates change.

📈 Early Withdrawal Penalty: Withdrawing funds before the term ends may result in a fee.

A CD can be a simple, low-risk way to grow your savings over time. Check with your community bank or credit union to explore available term options!

#CertificatesOfDeposit #SavingsStrategy #FinancialEducation #SmartSaving

EHL

When you see “Equal Housing Lender”, it’s more than just a logo. It represents a commitment to fairness in housing.

Here’s what that means:

🏠 Fair Lending Laws: Banks and credit unions follow federal laws, including the Fair Housing Act, that prohibit discrimination in housing-related lending.

🏠 Equal Opportunity for Applicants: Qualified borrowers cannot be denied or treated differently based on race, color, religion, national origin, sex, disability, or familial status.

🏠 Consistent Lending Standards: All applicants are evaluated using the same criteria and lending guidelines.

The Equal Housing Lender designation reflects a commitment to fair access and equal opportunity in housing for every qualified applicant.

#EqualHousingLender #FairLending #FinancialEducation #CommunityBanking #CreditUnion

Emergency Fund

Unexpected expenses happen. An emergency fund helps you stay in control when they do! Here’s what to know:

🚨 How Much Should You Save? A common goal is 3 to 6 months of essential living expenses. If that feels overwhelming, start smaller, such as a month of expenses or a set percentage of each paycheck.

🚨 What Counts as an Emergency? True emergencies are unexpected and necessary expenses like medical bills, urgent car repairs, job loss, or essential home repairs.

🚨 What Doesn’t Count? Planned purchases, vacations, or non-essential spending should be saved for separately.

🚨 How to Get Started: Set a realistic monthly savings goal and keep your emergency fund in a separate, easily accessible savings account. Better yet, set up automatic deposits for each pay period so your emergency savings can grow without you having to make a manual contribution each time.

Even small, consistent contributions can build a strong financial safety net over time!

#EmergencyFund #FinancialWellness #MoneyMatters #SmartSaving

Tax Refund

Receiving a tax refund can feel like a financial boost. Having a plan for it can help you make the most of it!

Here are smart ways to use your refund:

💰 Build or Boost Your Emergency Fund: Strengthening your savings can help cover unexpected expenses.

💰 Pay Down High-Interest Debt: Applying your refund toward credit cards, personal loans, or other high-interest balances may reduce long-term interest costs.

💰 Catch Up on Bills: If you’re behind on payments, your refund can help bring accounts current.

💰 Save for a Goal: Consider setting aside funds for a future expense like a home purchase, education, or major purchase.

💰 Invest in Yourself: Professional certifications, training, or skills development can pay off long term.

A thoughtful plan can turn a one-time refund into lasting financial progress!

#TaxRefund #FinancialWellness #SmartSaving

Pay-in-Full Discounts

Did you know some medical providers may offer discounts if you pay your bill in full? Here are a few tips to consider:

💡 Ask About Discounts: Some hospitals, clinics, and providers offer pay-in-full discounts — particularly for uninsured or self-pay patients. Even if you have insurance, it never hurts to ask if a discount is available. A simple phone call to the billing department could potentially reduce your total balance.

💡 Review Your Bill Carefully: Before making a payment, take time to review your statement. Billing errors can happen, including duplicate charges or services you didn’t receive. Requesting an itemized bill (a detailed breakdown of each charge) can help you better understand what you’re paying for and spot anything that needs clarification.

💡 Negotiate When Possible: If the total feels unmanageable, contact the provider’s billing office to discuss your options. In some cases, you may be able to negotiate a lower lump-sum amount or qualify for a financial assistance program based on your income. Many healthcare systems have hardship programs — but you often need to ask about them.

💡 Compare Payment Options: While paying in full may provide a discount, it’s important to consider your overall financial picture. A no- or low-interest payment plan might be more manageable and help you avoid tapping into emergency savings or taking on high-interest credit card debt. Choose the option that protects your long-term financial health.

Asking questions and understanding your options can help you make informed financial decisions!

#FinancialWellness #MoneyMatters #SmartSpending #FinancialEducation

Retirement Accounts

Saving for retirement doesn’t have to feel overwhelming. Understanding the different categories of retirement accounts is a great place to start!

📈 Employer-Sponsored Plans: Offered through your workplace and often funded through automatic paycheck contributions. Some employers may also offer matching contributions. Common examples include 401(k) plans, 403(b) plans, and pensions.

📈 Individual Retirement Accounts (IRAs): Personal retirement accounts you open independently. Traditional IRAs may allow tax-deductible contributions today, with taxes paid when withdrawals are made in retirement. Roth IRAs are funded with after-tax dollars, but qualified withdrawals during retirement are generally tax-free.

📈 Self-Employed Retirement Plans: Designed for individuals who work for themselves or run their own business. A common option is a Simplified Employee Pension (SEP) IRA, which allows higher contribution limits compared to many personal retirement accounts.

📈 Small Business Retirement Plans: Plans created for small businesses with employees. A SIMPLE IRA allows both employers and employees to contribute, helping workers build retirement savings through workplace participation.

The right option depends on factors like income, employment status, and long-term financial goals. Getting familiar with these account types can help you take the next step toward building long-term retirement savings!

#RetirementPlanning #FinancialEducation #FuturePlanning

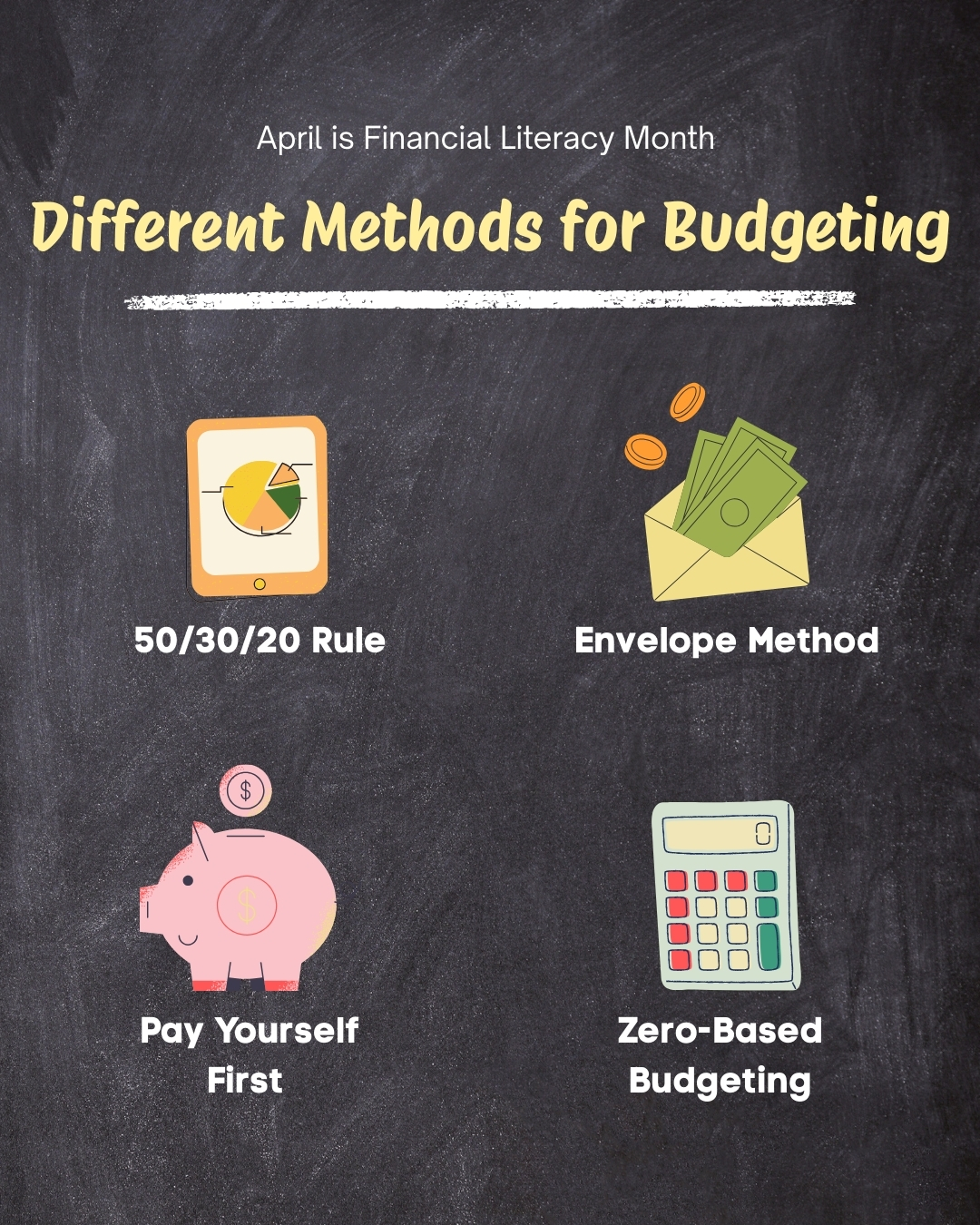

Budgeting

Budgeting doesn’t have to be complicated. Whether you follow the 50/30/20 rule or the envelope method, having a plan can help you take control of your money!

Here are a few different practical strategies to help you get started and build a budget that fits your goals:

📝 50/30/20 Rule: Divide your after-tax income into three categories—50% for needs , 30% for wants, and 20% for savings and debt repayment. This method provides a simple framework for balance.

📝 Envelope Method: Set spending limits for specific categories like groceries or dining out (some people store their budget for each category in actual envelopes). Once the allocated amount is spent, spending in that category stops. This approach encourages mindful spending and accountability.

📝 Zero-Based Budgeting: Assign every dollar of income a purpose so that income minus expenses equals zero. Every dollar is directed toward spending, saving, or debt repayment, helping eliminate unused funds.

📝 Pay Yourself First: Prioritize saving before covering discretionary expenses. Automatically transferring money into savings at the start of each month helps build consistency.

A clear plan makes it easier to stay organized, adjust when needed, and move confidently toward your financial goals!

#BudgetingTips #FinancialEducation #SmartSpending

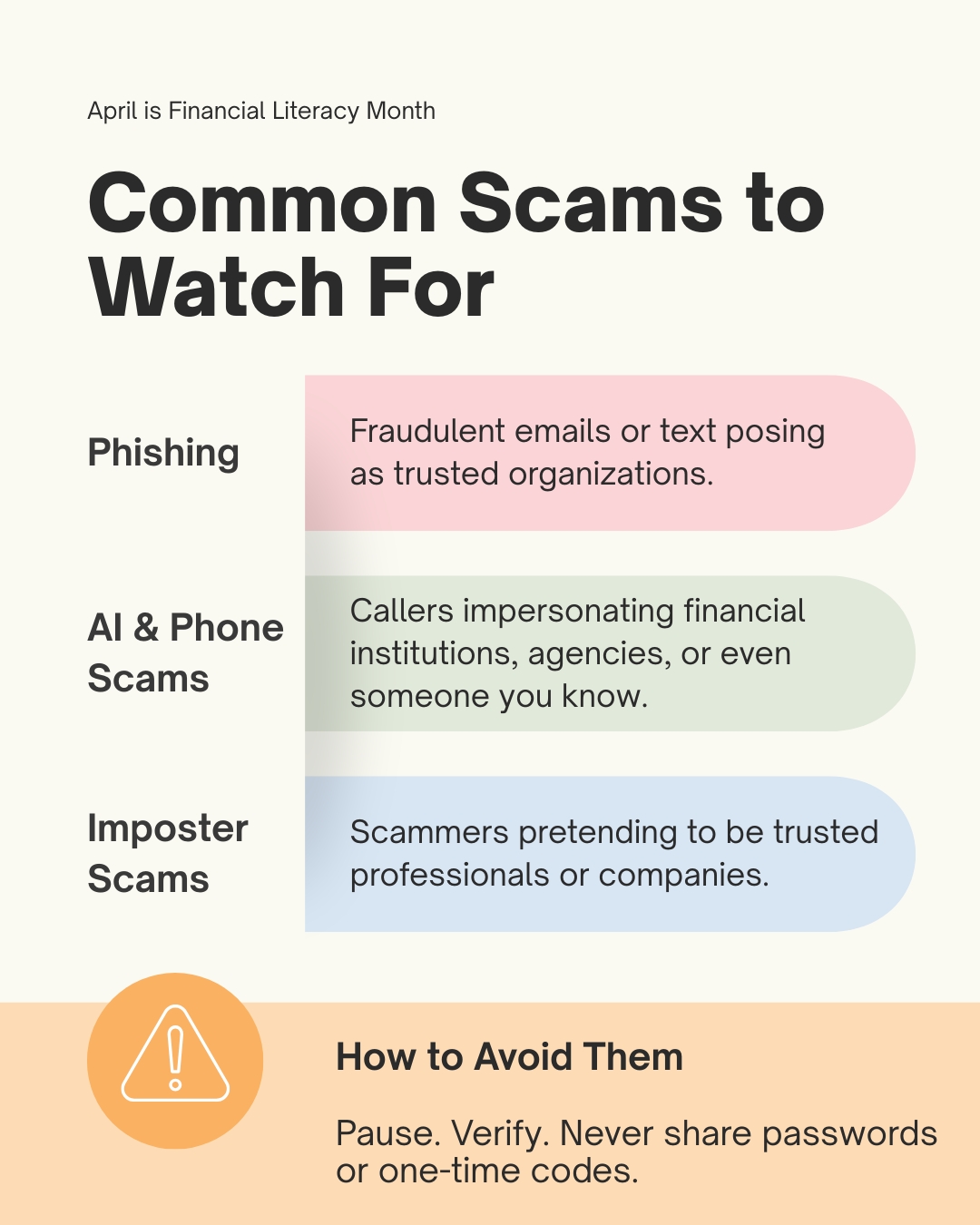

Scams

Scams are evolving—from phishing emails to AI-generated voice calls designed to sound like someone you trust.

Understanding the warning signs can help protect your money and personal information. Here are common scams to watch for and simple ways to avoid them.

Staying informed is one of the best ways to stay protected!

#FraudPrevention #ScamAwareness #FinancialSafety

Promote a Financial Literacy Event

This post layout is designed to help you promote an upcoming financial literacy event.

Here’s how to use it:

- Replace the placeholder image by overlaying it with your own promotional photo or image. You can do this easily in the Social Assurance Marketing Platform or in an editing tool like Canva.

- Update the event name, date, time, and location in the caption below.

- Add a brief description of the topics being covered.

Example caption layout:

We’re proud to support Financial Literacy Month by hosting an upcoming financial education event for our community!

What: [Event Name or Topic]

When: [Date & Time]

Where: [Location or Virtual Link]

Join us as we cover [brief description of topics such as budgeting, credit, homebuying, fraud prevention, etc.] and provide helpful insights to help you feel more prepared for making smart, financial decisions.

We look forward to seeing you there!

Credit Score

Your credit score plays a key role in financial decisions, from car loans to mortgages.

Understanding how it works can help you take practical steps towards strengthening your financial future. Learn the basics and simple ways to build your score responsibly!

#CreditScore #FinancialEducation

Financial Literacy Event Recap

This post layout is designed to help you easily recap a community financial literacy event.

Here’s how to use it:

- Replace the placeholder images by overlaying them with high-quality photos from your financial literacy event. You can do this easily in the Social Assurance Marketing Platform or in an editing tool like Canva.

- Update the placeholders in the captions below.

Example caption layout:

Thank you to everyone who joined us for [Event Name]!

During this event, we discussed [brief recap of topics covered] and enjoyed connecting with [students, local businesses, groups etc]. Together, we learned:

- [Key takeaway #1]

- [Key takeaway #2]

- [Key takeaway #3]

We’re thrilled to play a part in supporting the financial well-being of the communities we serve every day.